Synopsis: Product, politics, and the economy stalling the inevitable transition to EVs.

The true picture varies by region, and 2024 will likely see flat sales for EVs sales in the USA and much of Europe, but strong EV sales growth elsewhere including China. Globally, EV sales will still grow, but rather than exponential growth, what is expected globally is slightly lower growth than in 2023, driven by a significant slowdown in the USA and Europe, an acceleration in many markets where in the past very few EVs were available, and continued growth in China.

As suggested by the AI answer as quoted below, it depends on who you ask. The AI answer is really an answer focused on the US, and this page is looking at not just the US but the global picture, which provides another reason why it depends on who you ask, and this is in addition to the fact that those with opposing views interpret the same data differently.

In someways views are like the glass is half-empty vs half-full. It is not EV sales that are falling, but EV sales growth. Local factors in the USA and Europe, hit EV sales growth from late 2023 and could mean as much as 25% less growth global EV global in 2024 than in 2023, but globally, EV sales are generally growing, and it is non-EV traditional car sales that are more problematic.

However, politics, the economy and sensationalism lead to exaggeration of the slowdown and exaggeration of the “speedbumps” to slowing adoption both in the US and in Europe, as well as the speedbumps that present challenges for EVs in future.

While what is happening in each region, China, Europe, the USA and “the rest” is examined in more detail below, there are factors that affect EV growth everywhere, although the extent to which these factors for now, with some future problems looming for EVs , and EVs are still showing growth in market global share, led by gain in market share in China and “the rest of the world”.

A problem is that in USA and Europe the new EV products being introduced at this time are not compelling enough to bring sufficient new customers to sustain exponential growth.

Those stating sales are not stalling, quote sales statistics relative to previous years of 2021, 2022 and so far in 2023 which do show there is still real growth:

In fact, EVs overall are doing rather well, with sales projected to surpass 1 million this year — more than twice the number sold in 2021. Last year, total U.S. vehicle sales dropped by 8 percent, while the market for electric cars grew by 65 percent.

Politico: Are EV sales really slowing down?

Some promote the theory that the slowing of EV sales growth is because all the people who were willing to buy an EV already have now bought an EV. But consider, almost everyone who has bought an EV, did so only in the last around 7 years. Why didn’t they buy one 10 years ago? Mostly because the EVs of 10 years ago didn’t appeal to most of these people. The biggest selling EVs in most markets have been the Tesla Model 3 and Tesla Model Y, and before those vehicles were released the biggest selling EVs were the Nissan Leaf and far more expense Tesla Model S.

There were group of buyers for the Leaf and the Model S, and a bigger group of buyers willing to buy the Tesla Model 3 and an even bigger group willing to buy the Model Y. The problem right now, is that in most markets, there is no new vehicle(s) about to win over as many new converts as happen with the release of the Model Y.

The only reason EV buyers might have already bought, is a lack of new EV products to appeal to the next group of potential EV buyers. This is the biggest factor in slowing EV sales.

Secondly, different markets are also impacted by politics, and by media funded by those behind some of the politics.

Then, thirdly, there is the role of economics, with inflation, fears of recession, and a recovery of supply now Covid-19 has little impact, all contributing to price pressures and unsold internal combustion engine vehicles and electric vehicles.

These factors all combine, region by region to produce results that vary from strong EV sales growth through to stalling EV sales growth. Overall, globally EVs continue to increase market share, continue to progress in price competitiveness though Rights Law, and these factors combined does mean eventual market dominance of EVs still looks inevitable.

There is a reason for stalling in the USA, some other speedbumps in Europe, but in the world’s biggest markets of China and “the rest” the transition to EVs seems to be accelerating.

Background: Speedbumps of Product, politics and economics.

Product: Where is the next model Y?

The transition to EVs is driven by the release of compelling new products, or by price movements that increase appeal existing EV products.

EV sales will always be constrained while a percentage of buyers who can find an EV of their desired vehicle type that better suits their specific needs. For some vehicle types, a person still needs very specific taste before an EV becomes the best choice. While there are market segments, where depending on a buyer’s criteria, there are compelling EVs, but overall, in most countries, there is not yet enough compelling EV products. Ongoing releases of compelling EV products is the only way to keep increasing EV market share.

Two brands dominate in bringing compelling EV products to market: Tesla and BYD.

Outside China, at least until 2023, it was all about Tesla.

The volume products from Tesla are the Model 3, released in the US in 2017, Europe and China in early 2019, and to “rest of the world” markets from later in 2019 to as late as 2023 in markets like Thailand, and the Model Y began production in 2020 in the US and in China in 2021, in Australia in 2022 and in Thailand in 2023.

This means that markets with both Tesla and BYD brands well represented have the best prospects for EV sales growth in 2024.

Tough times for “legacy” car brands.

While Tesla and BYD make a profit from EVs across a range of price points, and Porsche, BMW, Mercedes and others are reported to make a profit on high end EVs, mainstream automakers faced with splitting product portfolios into a mix of EVs and gasoline/diesels are left with very small production runs of EVs and even reduced production runs of their traditional models.

This is one reason why the slowing EV sales story is more about Ford, GM and perhaps VW, rather than the entire industry.

Toyota predicts EVs will only reach 1/3 of new car sales, suggesting Norway, Sweden, China, Singapore etc have already gone too far, but even Toyota are a little vague on how long that 1/3 limit might apply.

Hyundai and Kia are seeing strong growth in EV sales, and BYD continues to grow. The lack of a new volume sales product will likely make it a tough year for Tesla growth, but while Tesla is facing more and more competition, it is from other EVs, which means EVs are still growing overall.

Politics.

The politics is mostly about protecting vested interests, in this case fossil fuel industries and the legacy ICE automobile industry.

The fossil fuel industry has a global market global influence and a huge budget to use to promote any suggestion that EV sales are falling or anything else that could slow the transition to EVs.

The situation with the legacy automobile industry is more complex, as particularly in the US, Germany, France and Japan, it also becomes an issue of jobs and the balance of imports and exports on one side and steps to address climate change on the other. This challenge of protecting legacy industry plays a key role in the transition to EVs in the US, Europe and Japan.

The fossil fuel industry then weaponizes any slowdown in the progress of EVs as a consequence protecting legacy industry into a bigger story about how EVs are not the future.

Economics.

In 2022, the world was still recovering from supply chain issues and many vehicles, both EVs and ICE vehicles, were in short supply. Prices for used vehicles soared in many markets as wait times for new cars could even reach a full year or more, and some new car dealers even charged premiums over and above the list price for new vehicles.

But by late 2023, for most new vehicles, substantial wait times became of thing of the past, inflation and cost of living factors all combined to see discounts for new cars return.

Stories of car yards full of new vehicles has become common in 2024, both for ICE vehicles and for EVs:

A backlog of vehicles is accumulating on dealer lots nationwide as, for the first time since June 2020, there are 80 days of new vehicle supply throughout the automotive industry.

Weak Sales Lead To Biggest Inventory Since Pandemic,

Politics, Economics, China and EVs.

At one time, many countries without their own automotive companies, had a tariff protected industry of local assembly of cars. For example, Australia had factories owned by companies including General Motors under the General Motors Holden subsidiary, Ford, Chrysler, Toyota, British Leyland and Mitsubishi. These locally assembled cars dominated sales because a tariff was applied to cars imported that were assembled outside Australia, with the locally assembled cars only being price competitive due to the tariffs. Gradually the tariffs on imported vehicles were lowered to allow better priced cars for Australians, and local assembly of cars in Australia dwindled until it finally ended in 2017.

China had a policy very similar to countries like Australia, with the additional requirement that local assembly companies were to be 50% joint ventures between the international automotive company and a local Chinese company. China removed the 50% joint venture requirement in 2018 for EVs, and 2022 for the wider car market in 2022, but the 25% tariff on vehicles not assembled in China remained. While Australian local assembly was hindered by a small domestic market and a not always competitive local manufacturing industry, China has a huge domestic market and highly competitive manufacturing. So competitive that Tesla, exempt from the JV requirements, as of 2024 exports cars produced in China by Tesla to the world other than North America.

Foreign automotive giants dominated the Chinese car market with vehicle produced by these joint ventures until around 2022 when BYD began to take the market lead from long term market leaders VW and Toyota. Until some recent withdrawals by foreign brands since 2022, every major automotive brand sell vehicles to the Chinese market at prices matching the lowest available worldwide.

BEIJING/SHANGHAI (Reuters) – China will scrap a limit on foreign ownership of automotive ventures by 2022 in a major policy shift to open up the world’s biggest car market, even as trade tensions simmer between Washington and Beijing.

In a move welcomed by Germany’s powerful car industry, China’s state planner said on Tuesday it would remove foreign ownership caps for companies making fully electric and plug-in hybrid vehicles in 2018, for makers of commercial vehicles in 2020, and the wider car market by 2022.

Reuters: 2018 China to open auto market as trade tensions simmer

Now it’s official, the government in Beijing has dropped the requirement for foreign car manufacturers to team up with a local joint venture partner – and sooner than expected. Specifically foreign firms making BEVs and PHEVs may begin selling in China this year.

Until this decision, foreign car manufacturers were forced to join a joint venture with a Chinese company before being allowed to do business on Chinese soil. That will change now.

Import tariffs in China for vehicles currently stand at 25 percent.

China drops JV requirements for foreign companies

Home charging: the elephant in the room.

This is a complex problem. The mistake is that even legislators tend to make the mistake of thinking charging an EV is like refuelling a gasoline car, when the reality is charging an EV is far more like charging a mobile phone. The simplest solution is to charge at night at home. The problem is that while almost everyone has a wall socket in a suitable location for charging their phone, as many as 50% of people have no wall socket available where they normally park their car, and public charging may be an economic opportunity for some, but it is no more viable in the long term as a real solution than commercial charging stations are real solution for people charging their mobile devices.

The global picture of EV sales: Slowing growth, complex reasons.

Global data: EVs Still growing, but as expected, not exponentially or homogenously.

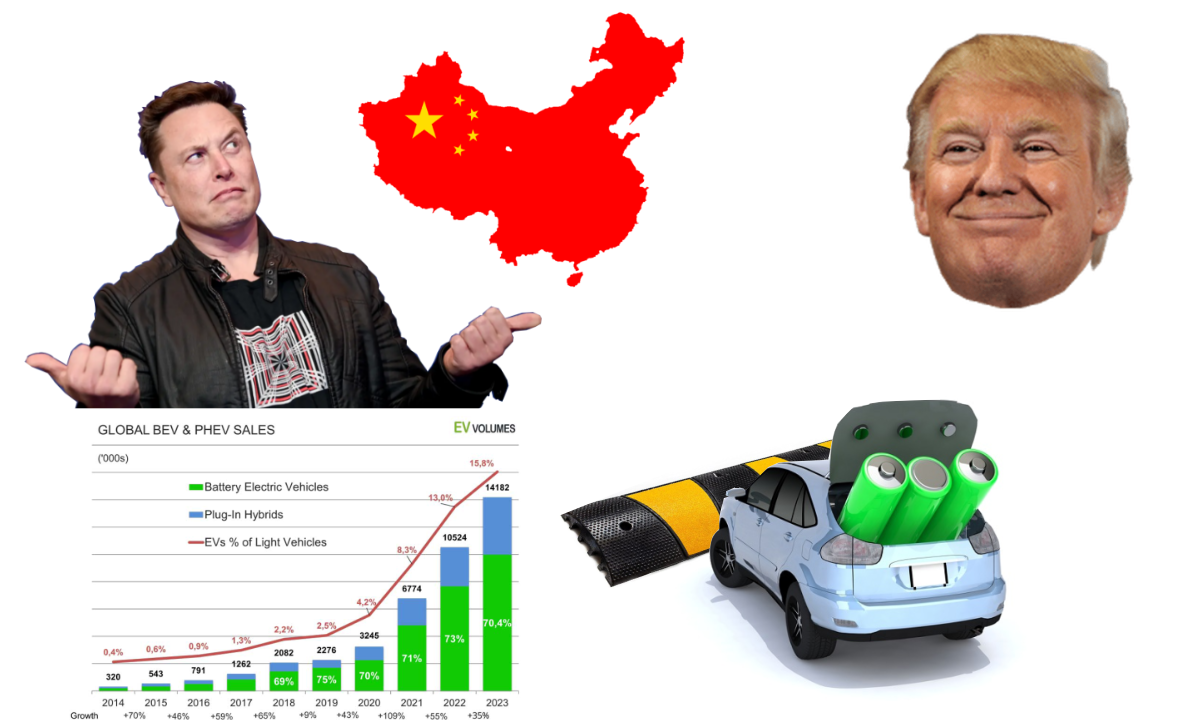

On IEA figures, global EV sales were 10 million in 2022, just under 14 million in 2023 and are projected to be 17 million in 2024. Globally, EV sales are still growing at a fairly constant rate, but not an exponential rate. The increase from 2023 to 2024, is now projected to be no greater than the increase from 2022 to 2023.

Despite many expecting that growth should always be exponential, continued exponential growth in a finite market would project growth to an infinite market share % instead of growth being limited to achieving 100% market share.

However, at low levels of market share, growth can be close to exponential, and any significant leveling off of growth at levels as low as at 20%, could mean a long and slow transition. Looking at projection I made around this time last year, numbers for Australia are in line with those projections, and China is even ahead of projections, but the latest data from the UK, Germany and USA are all well below those 2023 projections of market share in 2024.

While the overall result is consistent with the global from early in 2023, the results for USA and Europe are both behind expectations, while results from China and “the rest” either exceed or ahead of expectations. Since most reporting and web content comes from the USA and Europe, most people are hearing more about the slowing in the US and Europe, even though what happens in China alone has about double the impact of USA and Europe combined.

The projected 17 million sales numbers for 2024 are reported here:

Despite near-term challenges in some markets, based on today’s policy settings, almost 1 in 3 cars on the roads in China by 2030 is set to be electric, and almost 1 in 5 in both United States and European Union

News – IEA: The world’s electric car fleet continues to grow strongly, with 2024 sales set to reach 17 million

Results from 2023, and the split of sales by region is reported here:

While sales of electric cars are increasing globally, they remain significantly concentrated in just a few major markets. In 2023, just under 60% of new electric car registrations were in the People’s Republic of China (hereafter ‘China’), just under 25% in Europe,2 and 10% in the United States – corresponding to nearly 95% of global electric car sales combined.

Electric car sales neared 14 million in 2023, 95% of which were in China, Europe and the United States

Electric car sales1 saw another record year in 2022, despite supply chain disruptions, macro-economic and geopolitical uncertainty, and high commodity and energy prices. The growth in electric car sales took place in the context of globally contracting car markets: total car sales in 2022 dipped by 3% relative to 2021. Electric car sales – including battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs) – exceeded 10 million last year, up 55% relative to 2021.

IEA: Global EV Outlook 2023: Trends in electric light-duty vehicles

China Region: Strong growth despite the speedbumps.

While outside in the US and Europe a major “speedbump” is the lack of compelling new EVs with the potential to reach bestselling vehicle lists, BYD and others release new, often compelling, EVs in China every month.

As in many countries the Tesla Model Y is the bestselling vehicle, but 7 other EVs also make the top 10 list, and it is the depth of models which is what has enabled BYD to become the #1 car brand and overtake VW and Toyota.

Note the VW Lavida is basically a VW Golf with a boot/trunk and the Sagitar is similar to the Jetta.

While the Model Y is the bestseller, having only one other mass market model on sale, and no other vehicles in the top 10, means Tesla fails to even make the top 10 bestselling brands in 2023 in China despite having the top selling car.

The speedbump for EV sales in China in 2024 is the economy. The continued supply of new ever more competitive EVs ensures market share continues to grow, but consumer uncertainty means it could be a bigger share of a smaller market than that of 2023. With EVs or “NEVS” which also include both EVs and EV based plug in hybrids, having reached over 50% market share in Q1 2024, the economies of scale switches to favouring EVs which should accelerate pushing traditional ICE vehicles into ever smaller niche markets.

EVs sales will continue to grow in China in 2024, although it is going to be a tough and highly competitive market, with some brands losing out to the big EV players.

| # | Car (UK Sales) | 2023 | Q1-2024 |

| 1 | Ford Puma | 49,591 | 1 |

| 2 | Nissan Qashqai | 43,321 | 2 |

| 3 | Vauxhall Corsa | 40,816 | ? |

| 4 | Kia Sportage | 36,135 | 3 |

| 5 | Tesla Model Y | 35,899 | ? |

| 6 | Hyundai Tucson | 34,469 | ? |

| 7 | Mini | 33,385 | 8 |

| 8 | Nissan Juke | 31,745 | 4 |

| 9 | Audi A3 | 30,159 | 5 |

| 10 | Vauxhall Mokka | 29,984 | ? |

| ? | BMW 1 Series | 6 | |

| VW Golf | 7 | ||

| MG HS | 9 | ||

| VW T-Roc | 10 |

Europe: Yes, EV sales are slowing in Europe.

While Tesla and BYD both drive total global EV sales, BYD has very little traction in Europe, and it is hard to see a big change happening in 2024.

There is nothing new on the horizon in Europe from Tesla, it seems unlikely there will be big sales of BYD vehicles given European pricing, so what will drive any increases in European EV sales?

On the sales figures for the UK, the Telsa Model Y was 5th place for 2023, and dropped off the list for Q1 2024. All it takes to hurt quarterly Tesla sales is one delayed shipment, so the Tesla may be an aberration, but there no second big selling EV making the lists. Sales figure from Germany reveal a similar overall picture in terms of the types of cars leading the list, although leaders in each segment change. Interestingly, despite the Model Y being the bestselling individual car in Europe overall, it was #5 in Britain, #9 in Germany and #8 in France.

“Large SUV for on road use” is a segment totally dominated by the Model Y, and even though that segment is not bestselling segment in any EU country, it is the only segment where the same vehicle wins the segment in country after country.

For EVs to ramp up, what is needed is real EV contenders for best seller categories like small SUV and hatchback.

Most of the bestselling vehicles are categories similar to those in the top 10 in China, but while Chinese bestsellers, the BYD Dolphin and BYD Yuan Plus (Atto3), are also on sale in Europe and the UK, their price of those models in Europe/UK is too high for these vehicles to match the sales they have in other export markets like Singapore, Thailand or New Zealand.

So why are BYD vehicle in Europe price at a level too expensive to really compete? There is apparently a 5% tariff, but that does not explain why BYD cars seem to so far get a higher lift in price than others from China such as MG vehicles, or the Tesla Model 3. There have been suggestions that should BYD vehicles reach Europe at the prices they are reaching markets like Australia, the result could be devastating for some European car manufacturers, and it could be that BYD is being cautious, at least until they begin shipments from their EU based factory currently under construction in Hungary. China, as with many other governments around the world, provides a subsidy towards the purchase of EVs, and the scale of BYD in China means those subsidies have been applied to millions of BYD EVs, and as a result more BYD vehicles have received EV subsidies than any other brand in China, and even globally more subsides than any other brand other than Tesla. Certainly, the scale of BYD sales in China gives BYD a scale advantage.

For Europe, there is still no new Tesla since the Model Y, and without BYD cars at their relative pricing, no new EVs to really trouble top 10 selling vehicle lists. Hyundai/Kai, VW, Stellantis, and Renault all keep introducing EVs that are incremental improvements, but nothing to remarkable is yet arriving. BMW and Mercedes have EVs further up their range that can compete with any of the ICE vehicles, as does Porsche, but in the price bracket that can generate top 10 level sales, EVs from BMW and Mercedes are less competitive.

“The tipping point for combustion engines was last year,” Mertl, 49, said on a call with journalists, with regulation to cut carbon dioxide emissions capping any expansion. “Future volume growth will primarily come from battery electric vehicles.”

BMW saw strong EV orders during November and December, said Mertl, with demand in Europe set to keep growing. The manufacturer hasn’t seen any pullback, and expects the new i5 sedan and additional Mini brand EVs to boost sales, he said.

“The current sales plateau of combustion cars will continue and then fall off slightly,” he said.

BMW’s CFO Says ‘Plateau’ For Combustion Engines Is Here

At the same time, Mertl joins many industry colleagues in being more circumspect about future growth. That report says “the pace of demand acceleration for EVs has become less clear,” and as a result, BMW is predicting record electric sales for 2024 but at a slower rate than in previous years: it sold 14 million EVs and PHEVs last year globally but is predicting about 16.7 million this year. In past years, sales of plug-in cars have increased to the tune of 3-4 million per year.

But even so, BMW’s predicting a slowdown in annual EV growth for 2024

But even so, BMW’s predicting a slowdown in annual EV growth for 2024.

VW has an agreement to share technology with XPeng of China but not yet partner for Europe while Stellantis has become a major shareholder of Leapmotor and will import their vehicles and technology to Europe, but again, there is nothing announced that will give a major boost to EV sales in 2025.

In the end, the major European brand groups of VW, Stellantis and Renault appear to be not yet earning a profit from EV sales, so without the EV profit makers of Tesla and BYD to push them, why rush?

For politicians, why rush manufacturers into EVs if it might result if it could cost jobs?

The end of Germany ends EV subsidies, and Euro 7 from Brussels doesn’t seem to add up.

Another factor hitting EV sales in Europe in 2024 is the Germany suddenly cancelled the EV subsidy scheme, which was previously set to still apply throughout 2024, and this has already resulted in a drop in 1st quarter sales of EVs in Germany.

The budget constraints became official following a ruling by the country’s constitutional court to reduce spending by €60 billion euros. This forced the state to limit energy transition initiatives, including the EV subsidy, which was originally intended to apply until the end of 2024.

The initiative allowed German citizens to qualify for an EV subsidy based on the date of the vehicle’s registration. However, since registration can only occur after the vehicle is delivered, individuals acquiring an EV since January would be ineligible for the subsidy.

This also represents a major blow to the German mobility industry, as local manufacturers have been struggling with the transition into e-mobility. Although authorities targeted 15 million EVs on German roads by 2030, achieving this goal may be jeopardized due to budget constraints.

“This goal was already considered extremely unrealistic. Now it seems completely illusory,” said Ferdinand Dudenhoeffer, Analyst at the Center for Automotive Research, in an interview with the Rheinische Post newspaper.

Premature end of Germany’s EV subsidies triggers negative backlash

Another issue for Europe is the proposed new Euro 7 emissions standards.

As explained in the video here, a lot of work to comply with these regulations which are set to apply from July 2025. All the more incentive to sell ICE vehicles in 2024 and prior to July 2025!

In fact, generally regulations apply to the approval of cars for sale, and introduction of new regulations does not normal cancel approvals gained prior to the new regulations. It is usually simply impractical to require all cars already to be upgraded to meet new regulations, which means the regulations apply to new models seeking regulatory approval. However, any vehicle seeking regulatory approval after 2028, would have less than 7 years on sale prior to the EU 2035 zero emissions mandate, so Euro 7 could be a lot of work to make ICE vehicels saleable for a very short window. Regardless, it makes prior to July 2025 a time to focus on selling ICE vehicles!

USA: Yes, it can be argued EV Sales and Tesla are stalling in the USA!

Sales in the US are stalling, politics, EVs being transition to the NACS or Tesla standard charging plug, and lack of exciting new product in the main market segments all play a role.

Not only is the Tesla charging plug change having an impact on non-Tesla sales, but Tesla itself is also having something of a crisis!

Tesla has been slashing prices. Ford just cut the price of its Mustang Mach-E, too, plus it cut back production of its electric pickup. And General Motors is thinking about bringing back plug-in hybrids, possibly taking a step back from GM’s earlier commitment to shifting straight to pure EVs.

And now the EPA is considering slowing down requirements for automakers to sell more electric vehicles, dialing back what had been aggressive plans to move away from gas powered cars and SUVs.

To be clear: The American market for EVs is not collapsing. In the last quarter of 2023, EV sales were up 40% from the same quarter a year before, according to Cox Automotive. In fact, EV sales in the United States hit a record last year, topping 1 million for the first time.

But the EV market has nevertheless become a major disappointment. There is a troubling gap between expectations and reality.

CNN February 2024: How EVs became such a massive disappointment

Politics could be its own topic, but even if this doesn’t reflect what would happen under a Trump presidency, both Donald Trump and the US republican party at least have many fearing a Trump presidency would seek to undermine a transition to EVs and action on climate change. For example:

- Trump is attacking electric vehicles. Automakers already bet their future on them

- Trump’s Michigan speech: What he got right, wrong about EVs, China and the auto industry

- Trump’s Violent Language Toward EVs

What is clear is there is no declaration that a Trump presidency would seek to accelerate a transition to EVs, and there is the risk that there could be policy aimed at slowing EV adoption. All of this means both manufacturers and consumers have reason to be wary with their EV plans during 2024.

Then there is the move to NACS or Tesla type charging plug, which means effectively means EVs on sale at the current time, and for most if not all of 2024, will be sold with an “outdated” charging plug.

Then, the third point, a lack of new EVs in the market segments when Americans buy the most cars.

| # | USA-2023 Vehicle | Sales 2023 |

| 1 | Ford F150* | 750,789 |

| 2 | Chevy Silverado* | 543,319 |

| 3 | Ram Pickup* | 444,926 |

| 4 | Toyota RAV4 | 434,943 |

| 5 | Tesla Model Y | 385,900 |

| 6 | Honda CR-V | 361,457 |

| 7 | GMC-Sierra* | 295,737 |

| 8 | Toyota Camry | 290,649 |

| 9 | Nissan Rogue | 271,458 |

| 10 | Jeep Grand Cherokee | 244,595 |

| 11 | Toyota Tacoma* | 234,768 |

| 12 | Tesla Model 3 | 232,700 |

US Pickups and the Cybertruck.

The top vehicle segment in the US is pickup trucks, with 5 vehicles in the top 12 and sales of 2,269,539 units. This makes the biggest news for 2024 is that Tesla Cybertruck is now on sale! Well at least the US$102,000 and US$122,000 versions, as lower cost versions are not being delivered until 2025.

Plus, sales targets for the Cybertruck may not yet really boost EV sales in a big way.

Investment banks still have no idea how many Cybertrucks will roll off the line at Tesla’s Austin Gigafactory over the next two years. Goldman Sachs, Morgan Stanley, and UBS estimate that the marque will be able to build 48,500 units in 2024.

Robb Report Dec 2023: Some Wall Street Analysts Think Tesla Will Limit How Many Cybertrucks It Builds

The highest volume EV pickup so far, for the Ford F150 Lighting, which is available in 2024 at prices starting for less than half of the lowest Cybertruck 2024 price, Ford sold only 24,000 “Lightnings” in 2023, and is reported to be cutting production in 2024.

Ford sold just over 24,000 Lightnings last year, up 55% from 2022. But dealers are reporting slower sales and rising inventories on the electric truck, which starts at just under $50,000.

Ford cuts production of F-150 Lightning pickup on weaker-than-expected electric vehicle sales growth

Despite the pickup truck segment attracting all major pickup truck brands with the exception of Toyota to release a product, EV market penetration of the segment is well below the around 200,000 sales number required to match the overall USA EV market share. In all fairness, it is too early for a verdict on success of the GM pickup.

The Tesla Cybertruck does not appear yet ready to become a market leader, and the only other new Tesla product for 2024 might be the Robotaxi product, which, given there are still regulatory hurdles, is unlikely to create a sales bonanza in 2024.

Without new products, Tesla has been losing market share:

The year 2023 is behind us, and with the search for sales data ending for the year, it’s time for a summary.

U.S. Non-Tesla BEV Sales Surged In 2023 (insideevs.com)

All-electric car sales in the United States increased quite significantly in Q4 and in 2023, reaching new record levels. In today’s post, we will focus on the non-Tesla battery electric vehicle (BEV) sales, which were a major engine of growth.

Electric vehicle (EV) sales growth in the U.S. continues to slow, according to sales data analyzed by Kelley Blue Book. In the first quarter of 2024, Americans bought 268,909 new electric vehicles, according to Kelley Blue Book counts. EV share of total new-vehicle sales in Q1 was 7.3%, a decrease from Q4 2023.

April 11 2024: EV Sales Growth Slows; Market Leader Tesla Stalls

Overall, no clear new vehicle with the potential to repeat the success of the Model Y in a new segment has yet been announced.

The “rest”: The “long tail” of the world outside China, Europe and the USA.

Market size: “the rest” is a bigger vehicle market than USA or Europe.

It is easy to overlook “the rest”. Total the global EV sales outside China, Europe and the US in 2023 accounted for only 5% of all EV sales, but almost 69% of the world’s population. While population numbers are not exact, and definitions of “Europe” can differ from those used for vehicles statistics, as of early 2024 8.1 billion minus China at 1.4 billion, USA at 0.335 billion, and Europe at 0.740 billion leaves 5.625 billion people.

Using sales figures for not just EVs but all vehicles, “the rest” represents total 22.76 million of the global vehicle sales of 81.6 million in 2022) and 21.09 million of the 65.27 total global passenger vehicle sales in 2023, “the rest” represents at around 28% of the world global vehicle sales and 32% of passenger vehicle sales.

This means “the rest” is a larger market for vehicles than Europe or the USA, and almost as large a market as China.

It would be easy to assume that “the rest” comprises mostly countries where people own less cars and thus can’t afford EVs, but while car ownership is lower on average for “the rest”, low car ownership also once applied to China, which is now the world’s biggest car market. Plus, in China, at the low end of the market, there are EVs that sell for less than ICE vehicles.

OK, so now why so few EVs sales so far?

There are at least 3 key reasons.

Firstly, while the US and Europe are effectively large “single markets”, the rest is not one market, but a “long tail” of smaller markets, and none of those markets individually offers the scale of Europe or the USA, despite collectively the overall market size of the “rest” being larger than Europe or the USA markets. With new the introduction of new products, such as EVs, it is easiest to start with only the very largest markets.

Secondly, many EV brands, including Tesla, have started with higher end EV products that have mostly been sold a prices significantly higher prices of ICE vehicles, making them “premium products”, which have meant EVs are targeting only a small segment of the market in each market of “the rest”.

Thirdly, while BYD and some other Chinese brands do also focus on EVs at price points at and below that of ICEVs, BYD and most other Chinese companies have been mostly up until very recently been too busy with market opportunities in China to expand elsewhere.

For BYD and other Chinese brands with low priced products in their portfolio in particular, “the rest” is a mostly untapped market for EVs with the potential for even higher sales numbers than China. Just targeting 1/3 the current EV ownership rates present in China result in another market as large as China and larger than Europe and the US combined. I recall an old story of two shoe salesmen returning from Africa, with the first declaring, “there is no market, they don’t wear shoes” and the second “the market is wide open, they don’t yet have shoes”. In reality, “the rest” is very diverse and includes Australia, Canada and New Zealand, Latin America including Brazil, Mexico and Argentina, Asia including South Korea, Thailand and Japan, the Middle East and Africa.

With the exception of Japan and South Korea, “the rest” includes countries with no motor vehicle export industry to protect, which means, unlike the US and Europe, all EV brands could become available.

BYD in particular could make significant gains in “the rest” during 2024, with factories in Brazil and Thailand operational, and factories in Indonesia and Mexico planned.

While this will be further explored in future, “the rest” could be one of the key areas for EV sales growth in 2024.

The AI Answer to “are sales of EVs really slowing?”

On October 27th, 2023, I asked Microsoft AI “are sales of EVs really slowing?” and this was the answer:

The user query is about whether EV sales are slowing. The web results are contradictory and show different perspectives. Some sources suggest that EV sales are growing far more quickly than the overall market12, while others indicate that the supply of EVs is exceeding the demand3or that some companies have lowered their expectations for EV sales4. The summary should acknowledge the conflicting information and provide some possible reasons for the discrepancy. EV sales are slowing is a query that does not have a clear answer, as different sources report different trends and projections. Some sources claim that EV sales are booming and outpacing the overall market12, citing the increased consumer interest and environmental awareness. However, other sources point out that the supply of EVs is too high for the current demand3, leading to lower prices and incentives. Additionally, some sources note that some companies have revised their EV sales targets downward4, due to the challenges of battery supply, infrastructure, and competition. Therefore, the query may depend on the region, the time frame, and the type of EVs considered.

Learn more: 1.eenews.net, 2.politico.com, 3.ttnews.com, 4. cbtnews.com

Sept 2024 Progress check: 18 months of waning enthusiasm?

In a new report out this week, Morgan Stanley’s auto-industry analysts say to expect the global EV slowdown to persist another 12-18 months. Around 2027, however, they expect a “resurgence” in EV momentum.

What’s important to note about this “slowdown” is that it’s a drop in the rate of growth—not a decline in overall sales. Amid all the gloomy headlines, it’s easy to miss that more and more people are buying EVs. Morgan Stanley notes that the world is headed for yet another record year of electric sales. The bank’s analysts have an interesting take on what’s causing the slowdown and the keys to fixing it—maybe a Ford/Xpeng collab?—so let’s dive in deeper.

The EV Slowdown Will Last Another 12-18 Months, Analysts Say

As Alex Guberman says, part of the story is that EVs are just not that new anymore. However, another part is that what could be new, a battery breakthrough that brings fundamental change to battery capacity of EVs, just has still not happened. Things being just not that new also extends to climate change, where despite warming being more worrying that ever, the general mood at this time seems to be that it is just stale news, so cars could continue as they are forever. Of course, cars are not just continuing, and the transition is happening, but again, that is no longer news, whereas EVs not succeeding would be news.

Updates:

- 2024 September 9 : progress check on waning enthusiasm.

- 2024 April 30: Second draft edition.

- 2023 Oct 27: First draft on the basis of data showing a slowdown approaching.