I heard someone ask, “if EV (Electric Vehicle) sales continue to increase exponentially at the same rate, how long before all sales are EVs”? While exponential growth is no more sustainable for EVs than for anything else, the underlying statistics and real answer made me realise, EVs will probably reach an tipping point as soon as next year, and the shockwaves will be huge.

- Answering The Question.

- The tipping point and the stats.

- What Will Boost Sales?

- What Will Constrain And Limit The Market?

- An End To EV Subsidies? Or A Rethink?

- Current Subsidies.

- Automobile taxes vs subsidies.

- The Shockwave And Implications.

- China, Japan, Germany, USA.

- Established Brands And Automakers.

- Hey! Not So Fast! Limits And Roadblocks To EV Sales.

- Perspective, Pricing.

- The Grid, Lithium, Chargers.

- Conclusion.

Answering The Question.

The perhaps rhetorical question of “tell us how long it is going to take for Germany to get to 100% EVs if we are already at 30% if the triple every 12 months.” Of course in theory that would be 1 year, 1 month and a few hours, but that maths makes no sense as a from that point onwards later EVs are over 100% of the market. Exponential growth always hits an end point, and with market share breaks down as a principle from around 10% percent. What can work is declining market share. So if non-EVs went from 90% to 70% in one year, in another 2 years they would be at 42%. In Germany, this would likely be possible.

The same happens when looking at the data from UK and China markets, where for both markets, within 2 years on the current trend of decline in non-EV sales, ICE vehicles will become the minor players in a market dominated by EVs.

Just 6 months ago I wrote that in 2021, EVs simply don’t add up for most people, and now it is clear we are within 1 or 2 years of EVs being chosen by most people buying a new car. But consider the UK. In April the lowest cost EV was the MG ZS EV. Since then, a new updated version has been announced with improvements and a longer range for a lower price, and despite this, it is the MG is no longer the lowest priced EV in the UK. Prices are falling and specifications are improving.

The tipping point and the stats.

What Percentage Is A Tipping Point?

My ‘gut feel’ was to consider 50% of new vehicle sales being EVs as a tipping point, as this is when most people buying a new car are choosing an EV. From that point, the ‘normal’ purchase of a new car is an EV.

Buying a new new car in a market where 50% of purchases are EVs, is market where it is going against the trend to buy anything but EV.

If fact the data from Norway suggests 30% was the tipping point, with each additional 20% of market share requiring close to 1 additional year.

The sample is small and the three are many other factors that could explain the acceleration in uptake, but what Norway does prove is that is can happen.

It is now November 2021 and I have collected sales figures for the most recent month I have found for: UK, Germany, US, China, Norway, Sweden, New Zealand, Australia. Note, these are current month figures, which can be substantially above year to date numbers as market share in all market has risen substantial during the year.

Growth for EV sales in the top-15 markets was +74 %, while total passenger car markets were down -22 % combined compared to October last year. The resilience of EVs against market downturns and component shortages continues.

ev-volumes.com

What Might Boost Sales To Reach 30%?

EVs In Main Market Segments.

It turns out that many markets are at or about 20% EV market share already, but with the exception of China, in almost all markets, their are no EV models on sale in the normal leading market segments for new vehicle sales. For example in the UK, the Tesla Model 3 was sales leader of not just EVs but all vehicle sales in September 2021, despite the top selling cars in the UK normally being hatchback from the car segment at least one size smaller.

In markets such as Australia, New Zealand and the USA, ‘pickups’ are the top selling models, and while electric versions are coming, none have been on sale.

Within the next 12 months, this will change significantly with a far wider range of electric vehicles, including the Tesla Model Y arriving to join popular market segments.

Lower Cost EVs.

The other problem is that EVs are still only offered in price segments well above the average new car price. If you are buying a Porsche, then the most attractive vehicle is the Taycan EV, unless of course you are buying a Porsche SUV, in which case their is no Porsche SUV EV offered yet. But, just as with a Porsche SUVs, if you are buying a compact car, there are currently very few electric options, and unlike with more expensive cars, none at all at an equivalent price, unless you live in China. Outside China, the more compact cars that are on sale tend to be conventional gasoline models modified as and EV, and these are generally very costly.

In the next 12 months, many Chinese EVs such as the BYD Dolphin which are priced to compete with a Toyota Corolla, will reach more markets. In China, EVs sell for as little as US$5,000 and can be less expensive than equivalent internal combustion engine vehicles, but the coming flood of EVs from China is yet to hit.

What Will Constrain And Limit The Market?

While lower cost EVs are coming, they are not here yet, and perceptions take time to change. A major problem is that EVs work best when you can charge at home, and in most countries around 50% of motorists do not have that option. In fact, who cannot charge while parked at home 50% may often be an underestimate in many countries.

Charging infrastructure, and specifically infrastructure to allow charging at home, and without paying a premium to a charging network operator, can be a major constraint.

An End To EV Subsidies? Or A Rethink?

Current Subsidies: Hit And Miss In Addressing Need.

How can subsidies to purchase an EV continue once 50%, or even 30% of new car purchasers are buying an EV? This becomes government subsidies for the purchase of a car. So far, in many markets, these become government subsidies for the purchase of an expensive vehicle by people of above average income.

True, most subsidies are in the form a specific fixed amount, and as such do have greatest impact on the price of lower cost vehicles. The lower cost the vehicle, the more significant percentage that fixed amount becomes, but that helps little while there is a shortage of lower cost electric vehicles available.

In the US, there are no subsidies currently available on Tesla vehicles, but in the market segments Teslas are offered, these vehicles are already competitive.

Identifying Needs: Step By Step.

Background.

A challenge is that moving to electric vehicle involves brining in new technologies, and the established pattern for the automotive industry is to introduce new technologies first into expensive vehicles, and gradually the new technology then trickles down into lower cost vehicles, after some cost amortisation through sales of expensive vehicles.

Step 1: Kickstarter Subsidies To Get EVs To Early Adopters.

The very first EVs “new wave” EVs were produced purely to create environmentally responsible vehicles. They were not fun, largely impractical, with a high price for a boring, impractical vehicle.

Subsidies were introduced to try to find a niche for these vehicles, and to enable vehicle prices to fund the new technologies that initially did not have sufficient consumer appeal.

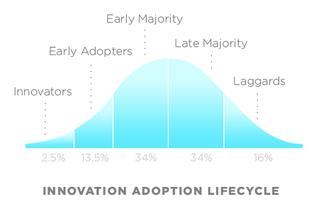

Step 2: Crossing The Chasm.

There is a model of adoption of new technologies made popular by Geoffrey A. Moore with different consumer types adopting technologies at different rates.

A challenge is that consumers in different countries and market segments of the car industry, are at a different points on the bell curve. Many markets are already into the “early majority” that will take EVs into being “normal” choices where subsidies no longer make sense, while some others at still at the “innovators”.

As countries reach around 18% and are into the early majority, it makes sense for “subsidies” to shift focus from subsiding purchasing EVs, to subsidising living with EVs.

Note that EV prices are effectively falling, so an EV subsidy that amounts to 10% of purchase price can become unnecessary within one year if prices can fall by 10% in that year.

Step 3: Social Justice and Infrastructure.

Once EVs start to become mainstream purchase choices, it makes more sense for governments to focus on delivering a quality experience for all from living with an EV, rather than subsidizing purchases, particularly as prices begin to undercut many internal combustion engine vehicles anyway.

Internal combustion engine vehicles have been part of society for around 100 years, and have played a role in structing where people live, how their homes are build, and how our cities, towns and suburbs are designed. Making a vehicle electric changes what it does best, and particularly how it is charged, and where it should be parked.

When we build a new airport or upgrade an existing airport, there can need to be compensation for those affected by the change. This same type of situation applies with EVs, with access to charging whilst parked, without paying a premium, becomes a social equality issue.

Sin-Tax Problems.

Generally, if a product is a major sponsor of sport, or was until it was until it was banned from advertising, then it is considered an undesirable, and may attract taxes that governments claim are in place to help moderate consumption. Think cigarettes, alcohol, gambling….. etc.

But motor vehicles may also qualify for the category, as not only are they sometimes sponsors of sporting teams or coverage, but also can be subject to governments taxing fuels, or introducing congestion taxes, and even taxing the vehicles themselves. In Australia for example, cars above a certain price point a subject to a “luxury car tax”, which results in even such cars a people movers and pickups attracting a luxury tax, while no other goods such as a yacht or even million dollar watch, no matter how expensive, attract a similar tax.

So where do EVs stand in terms of taxes?

Two potential problems exist for taxes of EVs.

- A very well funded lobby group will lobby for taxes to slow adoption.

- Governments become ‘addicted’ revenues from taxes and be loath to drop taxes even when original goal becomes irrelevant.

The Shockwave And Implications.

China: Car Maker, EV Maker.

China is the worlds largest car maker, producing twice as many cars as the next largest car making country, the USA. Even more significantly, China makes around 75% or the world’s electric cars. As you can see, the Chinese market makes up around 60% of the world EV market, and not only are all cars sold in China made in China, China also makes all Teslas destined for Europe and Asia, as well as electric vehicles for worldwide sale by BMW, Volvo and others, in addition to Chinese brands such as BYD, Nio, XPeng, Great Wall Ora, Li Auto, HOZON Neta and many others.

Every car sold in China, EV or ICE, is made in China. Every BMW, Mercedes, Ford, Toyota, Honda, Mazda, Jeep, VW, Audi sold in China, is made in China. For every brand from outside China other than Tesla, cars are made by a local Chinese as a joint venture between the foreign brand such as between Mercedes and BAIC. The venture always allows for transfer on knowledge on manufacture to the Chinese partner, but in many cases, the Chinese partner now make more vehicles in total than the foreign partner.

, and a Chinese manufacturing partner such as company with the foreign is made by a Chinese joint venture partnership wi

Japan, Germany, USA: The Biggest Losers.

Toyota is so concerned about the job loses in Japan from the move to electric vehicles that it has even formed “team Japan” to help keep the combustion engine alive. There is more, see “Toyota: The Anti-Electric Vehicle Company” for details, but Toyota is calling out that progress is bad for corporate profits and lowering prices is bad for economic activity. EVs can be built with 1/3 of the labour hours of building an ICE vehicle or hybrid, and Toyota argues that would be disaster for jobs in Japan, and reality is an even bigger problem is that no Japanese auto maker is ready for the shift to EVs so all will lose market share. No Japanese auto maker will be unscathed by the coming wave, and few if any will survive at all.

Germany automotive companies are generally better placed than the Japanese, but not that much better. Tesla has built a plant in Germany that is about to go online and would see the industry remain in Germany even if existing companies were to die, and while some will, most will survive in some form due to the value of their brands, although sometimes it may be like Volvo cars, which is now Chinese owned.

In the US there are three traditional mainstream companies: Chrysler which is now part of Stellantis and no longer a true US company, plus General Motors and Ford. New EV companies in the US include Tesla, Rivian, Lucid, Fisker Faraday Future, Aptera and others, as well as Apple intending to launch EVs. Telsa and Rivian are already valued higher than Ford and General Motors.

For US, the picture is complex, as no doubt the existing brands will suffer, but this could be offset by new entrants.

Established Automakers Globally.

Basically Tesla is the only stablished automaker outside of China is ready to start manufacturing vehicles at scale, and so far even most Tesla production has been in China. Some non-Chinese brands have EVs, such as Ford with the Mustang, VW with the ID3 and ID4, Audis, Mercedes EV variants for some models and the EQS, some BMWs now, and Jaguar has the iPace to name a few, while the BMW iX3 and MG, Volvo and Polestar models all being made in China.

Given most EVs in the world are purchased in China, every major established brand from outside China already has joint venture factories in China, producing their more EVs than all their factories outside China. For all manufacturers with the possible exception of Tesla with their Berlin Gigafactory, the fastest way for any manufacturer to respond to an increase in EV demand, it is ramp up production in China.

China will dominate EV manufacturing over the next few years. While Europe could the respond and increase their EV manufacturing given time, when was the last time maufacturing was moved on significant scale out of China and to the West?

New brands from China and the US will take over half the global car market, and EVs will cost less, and last longer, require less labour to produce and service. Overall, the automotive industry of established players will drop below half of current revenues, and that will hurt many existing automakers. Some will not survive.

Hey! Not So Fast! Limitations and Roadblocks To EV Sales.

New Car Sales Take Years To Change What Is On The Roads.

Consider Germany, where EVs have just reached 30% of new car sales. Yet driving in Germany, you will not see many electric vehicles on the road. The average age of vehicles on the road in Germany is just under 10 years, which means that it would take 10 years of 30% of sales to reach 30% of vehicles on the road, and after 1 year of 30% there would be only 3% of electric vehicles on the road. While the current level of sales is around 30%, this is the peak for the year, and ytd sales are lower, with a total for all years so far in Germany likely to result in only around 3% of cars in Germany being electric at this time.

In the US the average vehicle age is over 12 years, while in Britain it is a relatively young 8.4 years.

The average age of the passenger car stock is quite stable. At the end of 2017 it was 10.5 years, compared to 10.6 the year before.

Statistics Norway.

So even in Norway, despite almost all new cars now being EVs, it will take another 5 years for half the cars on the roads to be EVs.

The Grid, Lithium, Recharging Points.

One claim is that the electric grid in many countries will not be able to cope with the additional load of electric vehicles. Statistics calculated by Forbes for the UK, show that if the UK was to be fully electric, an an additional 21% of power would be required by the grid. Given the fastest possible conversion of cars on the road, in the event all new car sales are electric, and cars last 8.4 years in the UK so only 12% of cars are replaced each year, the grid would need to increase in capacity by only 2.5% per year. During the 1960s and 1970s, the entire would was increasing population at close to this level of growth, so there is worldwide practice at growing grid power at this rate. In summary, grid power is not a real limitation.

A second claims is that the world does not have enough lithium to build all the batteries required. This one has some merit, despite there being no chance of actually running out of lithium, building all the batteries required and scaling production of batteries is a challenge. Consider the world currently being constrained by silicon chips, despite the entire earth’s crust being around 28% silicon. Clearly, there being ample amounts of a chemical element does not mean there is sufficient being mined at this time, or that there is sufficient manufacturing capability to convert the element into what we need made from the element. In fact not lithium, but cobalt, as used in Telsa NCA batteries or NMC batteries by most other brands, is a constraint for now, but with many brands switching to LFP batteries for some or all of their batteries, the expensive constraining element is avoided. While after a 100 years of making lithium batteries and not recycling the lithium we could face a scarcity, batteries will be recycled, at least as long as we use lithium. Even aluminium batteries, would likely be recycled, and aluminium is the third most common element in the Earth’s crust. So, we wont run about of ability to make batteries, but ramping up manufacture is a constraint in the short term.

The third claim is that the ability to recharge will be a constraint. Again, this could be real, but because of insufficient public charging stations, but because too many people are currently unable to charge at home.

Conclusion.

EVs adoption is accelerating, and after taking such a long time to get started, may not happen far faster than legacy car makers, or society, is ready to handle.